")

Mananya Kaewthawee/iStock through Getty Photos

Paysafe Restricted (NYSE:PSFE) is a fee processor. The corporate has had a troublesome time as Paysafe’s debt load is consuming into the corporate’s complete working revenue and the corporate has needed to write off its belongings. I imagine the corporate’s underlying money flows are barely higher than the corporate’s earnings which traders can belief, which is why I’ve a score on the inventory.

Firm

Paysafe operates underneath a number of manufacturers, equivalent to Paysafecard, Revenue Entry, Neteller and Skrill. Many of the firm’s manufacturers are fee platforms. For instance, Skrill processes international funds, facilitating cash transfers between nations and currencies. Revenue Entry, then again, is an affiliate marketing online software program answer, largely utilized by on-line playing web sites:

IncomeAccess Shoppers (incomeaccess.com)

Playing companions are additionally essential for Paysafe’s fee platforms equivalent to Neteller and Skrill – many playing websites provide deposits and withdrawals via these platforms.

Because the firm went public, it has worsened the worth of traders’ investments, because the inventory is down 90% from late 2020 ranges:

Paysafe Inventory Chart (On the lookout for Alpha)

There appears to be no finish in sight to the decline, as the corporate’s year-to-date efficiency is -34%.

Funds

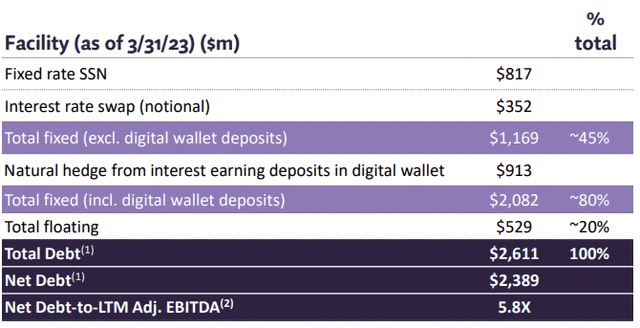

Paysafe’s steadiness sheet may be very worrying – the corporate holds $2,611 million in long-term debt, of which $10 million is in present debt. A lot of this debt is in interest-earning deposits in clients’ digital wallets:

Paysafe Money owed (Paysafe Q1 2023 Earnings Presentation)

The corporate has $222 million in money, which places the corporate’s web debt at $2,389 million – in comparison with Paysafe’s market cap of $689 million at a share value of $12.04, I imagine that is an unhealthy quantity.

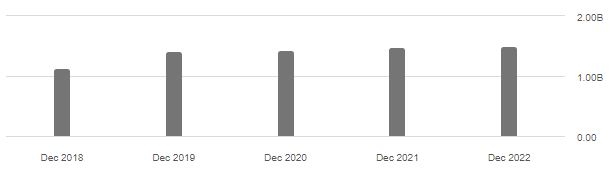

Paysafe’s revenues grew barely at a compound annual fee of seven% from 2018 to 2022:

Revenue (In search of Alpha)

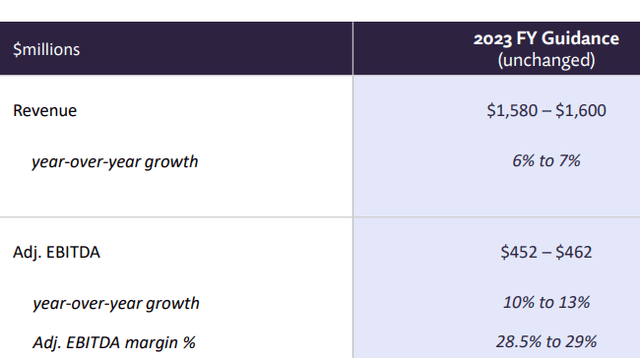

This has been fueled by the acquisition of viafintech and Safetypay – the corporate doesn’t seem like rising organically, which ought to fear traders. The corporate continues to be on observe for development of 6-7% within the present 12 months, with no M&A exercise within the final twelve months. This raises hopes that the corporate might develop organically sooner or later.

2023 Steering (Paysafe Q1 2023 Earnings Presentation)

The corporate’s working margin has declined through the years – in 2018, the corporate’s working margin was 14.2%, whereas right now it stands at 3.9% with the most recent numbers. Margins are displaying some indicators of enchancment, as in Q1 the corporate’s working margin was 9.1% in comparison with final 12 months’s 4.2% – steerage adjusted EBITDA development of 10-13%, greater than anticipated income development.

Paysafe’s money flows are nonetheless higher than their working revenue, which traders imagine. The corporate has a backlog of $261 million in goodwill amortization associated to the corporate’s acquisitions, worsening working revenue with out impacting money flows. The corporate has certainly had $147 million in intangible asset purchases over the previous twelve months, which has worsened money circulate. These investments do not present up in Paysafe’s working revenue, although, as the corporate’s 2022 depreciation is simply $6.5 million. In complete, the corporate’s money flows must be about $100 million higher than their EBIT would make them imagine.

All of those components add as much as the truth that curiosity prices are consuming into present earnings for shareholders – over the previous twelve months, the corporate’s EBIT is $59 million and curiosity expense is $138 million. I imagine that Paysafe ought to nonetheless be capable to handle its debt if enterprise doesn’t deteriorate, as Paysafe’s money flows are nonetheless fairly wholesome.

Upcoming Earnings

The corporate experiences its second quarter earnings on August 15. I imagine traders ought to maintain an in depth eye on the corporate’s income development – rising income would considerably enhance Paysafe’s enterprise as I imagine margins ought to develop with scale. Analysts at the moment count on development of 4.3% for Q2, together with adjusted EBITDA margin rising by a share level – the corporate’s income estimate is $395 million and adjusted EBITDA estimate is $111 million.

Valuation

Paysafe’s valuation may be very obscure because of the giant quantities of depreciation, write-offs and restructuring prices. A very powerful determine for my part is free money circulate – the corporate is at the moment trailing MCAP/Levered FCF – at a ratio of 5.43, under its historic figures:

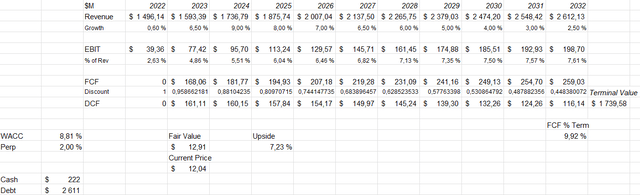

To additional show the estimate, I modeled the discounted money circulate mannequin as traditional. The estimation is kind of troublesome as a result of the corporate has such a major quantity of debt, however the mannequin offers some approximation.

For the estimates, I entered income development of 6.5% – which is the midpoint of Paysafe’s present steerage. Going ahead, I estimate within the mannequin that Paysafe’s development will speed up barely to 9% in 2024, with a sluggish decline to 2% in regular development. Moreover, I imagine the corporate ought to proceed to increase its margin via development – within the mannequin I estimate an EBIT margin of 10.21% for the corporate. These expectations make the DCF mannequin a good worth estimate of $12.91, which is 7% above the present value:

DCF mannequin of Paysafe (writer’s calculation)

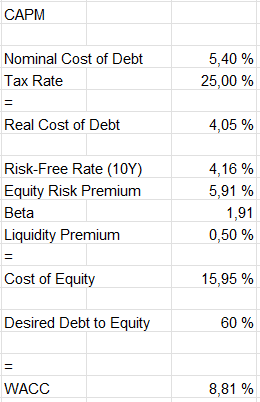

I used a weighted common value of capital of 8.81% within the mannequin, derived from the price of capital mannequin:

Paysafe’s CAPM (writer’s calculation)

Paysafe says its rate of interest is 5.4% with partially mounted curiosity debt, which I exploit within the CAPM. It is laborious to guess the long-term debt-to-equity ratio, however I am placing in a determine of 60% – if the corporate is ready to repay a few of its debt, I imagine that might characterize a medium-long time period installment.

I exploit the 10-year United States Treasury yield of 4.16% because the risk-free fee on the price of capital aspect. An fairness danger premium of 5.91% is Professor Aswath Damodaran’s estimate for the USA. I added a liquidity premium of 0.5% to handle inventory liquidity.

The beta of the fee processor is 1.91 in line with Yahoo Finance. I imagine {that a} fee processor’s operations shouldn’t be cyclical in nature – particularly given the corporate’s positioning within the defensive playing trade. I attribute the excessive beta to the corporate’s great amount of debt, which leverages shareholder danger on account of financial downturns – if Paysafe manages to repay a good portion of its money owed, for my part, the beta must be considerably decrease going ahead.

For now, I’ve a beta of 1.91 within the mannequin, creating a price of capital of 15.95% and a considerably decrease WACC of 8.81% associated to the corporate’s great amount of debt.

Closing phrases

At $12.04 per share, I imagine Paysafe may very well be an excellent funding. The corporate’s future is dependent upon its skill to repay its at the moment giant debt. If enterprise improves with income development, the corporate might create worth for shareholders. Nevertheless, with the present elevated danger profile, I’ve a score on the inventory.